- My Forums

- Tiger Rant

- LSU Recruiting

- SEC Rant

- Saints Talk

- Pelicans Talk

- More Sports Board

- Winter Olympics

- Fantasy Sports

- Golf Board

- Soccer Board

- O-T Lounge

- Tech Board

- Home/Garden Board

- Outdoor Board

- Health/Fitness Board

- Movie/TV Board

- Book Board

- Music Board

- Political Talk

- Money Talk

- Fark Board

- Gaming Board

- Travel Board

- Food/Drink Board

- Ticket Exchange

- TD Help Board

Customize My Forums- View All Forums

- Show Left Links

- Topic Sort Options

- Trending Topics

- Recent Topics

- Active Topics

Started By

Message

re: Advice for relative - Over 75 with 401K

Posted on 5/22/23 at 12:25 pm to TorchtheFlyingTiger

Posted on 5/22/23 at 12:25 pm to TorchtheFlyingTiger

quote:

No offense, but if you're providing the advice and first instinct was withdraw it all and move to savings account, you shouldnt be offering any advice until you get informed. Seek a fee only fiduciary advisor that doesnt charge an assets under management fee. The relative did alright accruing $500k in 401k I'd guess they have at least a better clue what theyre doing than what you suggested right out the gate.

Wasn't my suggestion. It was a question that was posed to me. They had an old savings account that got updated to a 3% annual yield account and now they think that is great. I have no idea what they are looking for a this point. I'm a beneficiary but not part of a joint account. But I'm not the only beneficiary and I think another beneficiary is in their ear.

This post was edited on 5/22/23 at 12:26 pm

1

1

Posted on 5/23/23 at 8:56 am to DiamondDog

I paid for in home care for my mother for two years. It cost about $35,000 a year for someone at $15 an hour but she got to stay in her bed in her home until she died. Assisted living would have been 2-3 times as much. Most people don’t realize that if you request hospice care for an older patient the get everything paid for like hospital bed, toileting equipment, health supplies, meals, weekly home health check, etc. We had a great experience with hospice. My paternal grandfather died in a shitty Medicare rehabilitation facility after a stroke where he shared a small room built out of cinder blocks with a roommate. My mother was not going to do that on my watch.

Posted on 5/23/23 at 9:40 am to Tigerfan1274

In lieu of doing the drastic step of liquidating and moving to a savings account, could rollover to an IRA and buy CDs.

Schwab is currently offering 5+% CD rates FDIC insured (I think they even spread across institutions so you can protect more than $250k).

I cant fathom how anyone would be advocating withdrawing and realizing taxes all at once just to get 3% bank savings rate which isnt even locked in.

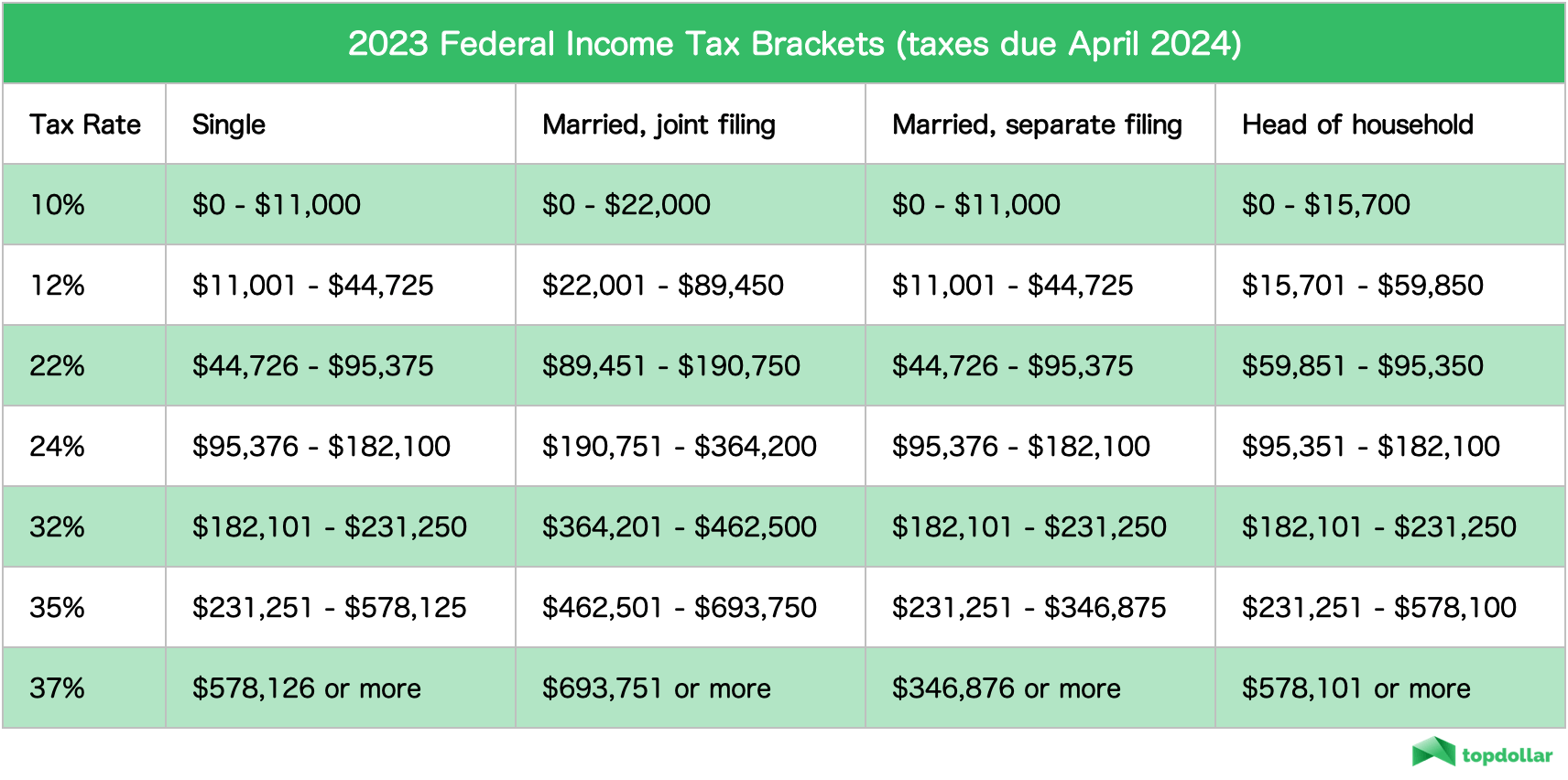

Just show them this and point out the massive tax hit. They'd be paying 30%+ on much of the withdrawal!

I'd try to work with the other family member to get them better informed and on same page. Otherwise, they may eventually succeed in convincing elder to to make a terrible mistake.

Schwab is currently offering 5+% CD rates FDIC insured (I think they even spread across institutions so you can protect more than $250k).

I cant fathom how anyone would be advocating withdrawing and realizing taxes all at once just to get 3% bank savings rate which isnt even locked in.

Just show them this and point out the massive tax hit. They'd be paying 30%+ on much of the withdrawal!

I'd try to work with the other family member to get them better informed and on same page. Otherwise, they may eventually succeed in convincing elder to to make a terrible mistake.

Posted on 5/24/23 at 8:37 am to WB Davis

I went a different route. I bought a LTC policy from a very strong company early on. I and my spouse each have a $300K benefit in today's dollars, compounding at 5%. I may die without using it, and hopefully will, but it should allow me to spend money without worrying that I will need it. It may not be enough to cover all of my expenses, but our other guaranteed income should easily cover it. Unfortunately, these polices are pretty expensive now, and it's a tough call.

Posted on 5/27/23 at 7:21 am to TorchtheFlyingTiger

Appreciate your input and the tax chart. Definitely going to have that handy if this comes up again.

Page 2 of 2

Page 2 of 2

Popular

Back to top