- My Forums

- Tiger Rant

- LSU Recruiting

- SEC Rant

- Saints Talk

- Pelicans Talk

- More Sports Board

- Winter Olympics

- Fantasy Sports

- Golf Board

- Soccer Board

- O-T Lounge

- Tech Board

- Home/Garden Board

- Outdoor Board

- Health/Fitness Board

- Movie/TV Board

- Book Board

- Music Board

- Political Talk

- Money Talk

- Fark Board

- Gaming Board

- Travel Board

- Food/Drink Board

- Ticket Exchange

- TD Help Board

Customize My Forums- View All Forums

- Show Left Links

- Topic Sort Options

- Trending Topics

- Recent Topics

- Active Topics

Started By

Message

re: Denmark raises retirement age to 70

Posted on 5/26/25 at 6:01 pm to kywildcatfanone

Posted on 5/26/25 at 6:01 pm to kywildcatfanone

quote:

Cut govt spending by 50% at all levels, and no sane person would notice.

Well to do this would require cuts to Medicare and social security so yeah they would

1

1

Posted on 5/26/25 at 6:30 pm to fallguy_1978

quote:

I believe it only matters when you start collecting. Imagine if y'all had be getting 7-10% returns on that money the last 20+ years. It's a rip off

It did a little reading and it looks like you have to max out the social security max for 35 years.

I’ve got 11 years in on that with 24 more years to 67

So technically it’s doable but I can’t see any way I’m still working at 67 full time. I may do something to stay busy and supplement my income but not full time grinding 5 days a week.

Posted on 5/26/25 at 8:31 pm to Rize

You only need 40 quarterly SS credits to draw (10 years). If you have you worked fewer than 35 years, zeros are used to fill in missing years. The way it is calculated, their are bend points where you get lower return on additional earnings anyway so not a poor return on additional years worked/higher income.

Posted on 5/26/25 at 8:34 pm to HailHailtoMichigan!

quote:

They are not afraid to tax the crap out of their middle classes, because they understand it’s where the taxable income is located.

That’s not where it is in this country. It’s in the top .01%.

And the middle class already pays the highest marginal rate here because they are typically W2 earners who don’t own businesses or significant real estate.

This post was edited on 5/26/25 at 8:38 pm

Posted on 5/26/25 at 8:48 pm to HailHailtoMichigan!

quote:

The Scandinavians may have the wrong model of economic stewardship overall, but at least they understand how to *fund* their system. They are not afraid to tax the crap out of their middle classes, because they understand it’s where the taxable income is located.

Sure, tax the crap out of the middle class until it’s gone, very Marx-like.

Posted on 5/26/25 at 8:53 pm to HailHailtoMichigan!

The dirty truth is governments don't want to pay anyone their retirement benefits.

The goal is to milk you your entire life as long as absolutely possible then ideally for them you drop dead right after you retire.

People living into their 80's and 90's was never part of their plan.

The entire thing is a ponzi scheme which can only keep moving forward as long as most people die before collecting their benefits.

The goal is to milk you your entire life as long as absolutely possible then ideally for them you drop dead right after you retire.

People living into their 80's and 90's was never part of their plan.

The entire thing is a ponzi scheme which can only keep moving forward as long as most people die before collecting their benefits.

Posted on 5/26/25 at 10:32 pm to LSUtoBOOT

I wonder what percentage of their spending is on social security? And what the inflows of immigrants did to their budget?

Posted on 5/27/25 at 7:24 am to fallguy_1978

quote:

maybe remove the income cap on social security,

Why, will my benefits be going 100% to match all that over the cap taxation being levied upon me? I quite like my summer "raise" each year when I cap out. I'm not going to get shite anyway; it will eventually be means tested and I'll be too "wealthy" to even recoup what I wasted putting in.

Posted on 5/27/25 at 9:08 am to HailHailtoMichigan!

quote:

but at least they understand how to *fund* their system.

They wouldn't be having to raise the retirement age if they knew how to fund their system properly.

Posted on 5/27/25 at 9:09 am to mule74

quote:

middle class already pays the highest marginal rate here

Arguments around marginal rate are meaningless. And the middle class absolutely does not pay the highest marginal rate. Or effective rate.

This post was edited on 5/27/25 at 9:19 am

Posted on 5/27/25 at 9:44 am to HailHailtoMichigan!

They’re not even trying to hide it anymore. Most of the money we put into “social security” along with the amount our employers pays into our accounts will never be realized in our lifetime.

Posted on 5/27/25 at 12:04 pm to GoCrazyAuburn

quote:

Arguments around marginal rate are meaningless. And the middle class absolutely does not pay the highest marginal rate. Or effective rate.

In what part of your mind did you make up those numbers?

Posted on 5/27/25 at 12:12 pm to mule74

quote:

In what part of your mind did you make up those numbers?

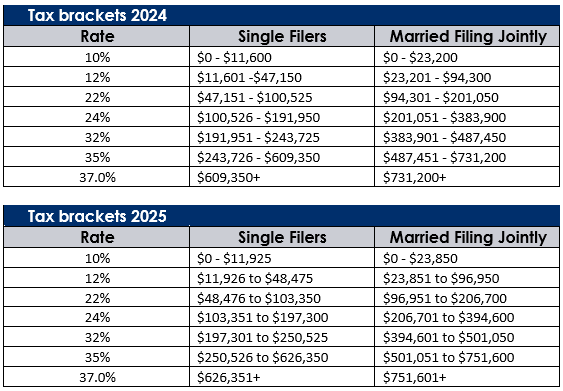

Since you stated marginal, here you go:

Which one of those are you defining as middle class?

Posted on 5/27/25 at 1:33 pm to GoCrazyAuburn

quote:

Which one of those are you defining as middle class?

I define classes based on net worth, not income.

The bottom 50% of America is the lower class. They control about 2% of net worth. The middle class is the 50%-90% range which controls about 35% of the net worth. The upper class is the top 10% which owns about 60% of the net worth.

Your initial post lauded the courage of European countries to tax the middle class because that this where the money is. I said that is not true in the United States, and it is not. The upper 10% controls 60% of the money and the top 1% controls 30%. That is where the money is.

You posted an income tax bracket. Back to my initial point, people in the top 1% of US earners (and especially the top .01%) are earning much of their money outside of a W2. They are not subject to the taxes you posted above.

So, while yes, someone earning a $1mm salary is paying more than someone earning $200,000 on W2 income, the person earning $1mm is more likely to accumulate assets that will be taxed at a lower rate and is more likely to take advantage of specific tax breaks that are not available to lower earners.

The effective tax rate of the top 1% of net worth holders is only 26%. Perhaps I should have said effective rather than marginal. I stand by my original point. Taxing the middle class (however you or I define it) will not move the needle. The top 1% is where the money is.

Posted on 5/27/25 at 2:03 pm to mule74

quote:

I define classes based on net worth, not income.

Kind of an illogical thing to do when discussing income taxes.

quote:

The bottom 50% of America is the lower class. They control about 2% of net worth. The middle class is the 50%-90% range which controls about 35% of the net worth. The upper class is the top 10% which owns about 60% of the net worth.

quote:

Your initial post lauded the courage of European countries to tax the middle class because that this where the money is

I'm sorry, what? My initial post with you was in response to you. I did not laud anything, just pointed out that your post was wrong. My first post in the thread actually criticized them. Maybe go back and read what I posted?

quote:

You posted an income tax bracket. Back to my initial point, people in the top 1% of US earners (and especially the top .01%) are earning much of their money outside of a W2. They are not subject to the taxes you posted above.

Ah, I see the problem. You used marginal rate when you actually meant effective rate, while talking about defining middle class by net worth while discussing income tax rates. Yes, who couldn't follow that?

Now then, since you want to talk about effective tax rates, you are still wrong. The middle class does not pay the highest effective tax rate either.

quote:

The effective tax rate of the top 1% of net worth holders is only 26%. Perhaps I should have said effective rather than marginal. I stand by my original point. Taxing the middle class (however you or I define it) will not move the needle. The top 1% is where the money is.

Yes, using the correct terminology is usually pretty useful. Now that we are usuing correct terms, the top 1 % pays 26 %, the top 5%-1% pays 18.8%, the top 10% to 5% pays 14.3%, the top 25% to 10% pays 10.7%, the top 50% to 25% pays 7.7%, and the bottom 50% pays 3.7%. That is the analysis from 2022 tax year, average effective rate paid.

At no point does the middle class pay a higher effective rate, no matter how you want to slice things. The rest of your assertion is just wrong. Raising taxes on the middle class definitely moves the needle. Saying otherwise is folly, regardless if it is the right or wrong thing to do.

This post was edited on 5/27/25 at 2:33 pm

Posted on 5/27/25 at 2:57 pm to GoCrazyAuburn

quote:

Kind of an illogical thing to do when discussing income taxes.

I am talking about all taxes. Not just income taxes.

quote:

the top 1 % pays 26 %, the top 5%-1% pays 18.8%, the top 10% to 5% pays 14.3%, the top 25% to 10% pays 10.7%, the top 50% to 25% pays 7.7%, and the bottom 50% pays 3.7%. That is the analysis from 2022 tax year, average effective rate paid.

Again, you are only referencing income taxes. I am referring to all taxes.

quote:

Most Americans receive almost all their income through wages and retirement income (pensions, 401(k)s, social security, and individual retirement accounts). The most recent available IRS data (2014) shows that wages and retirement income made up 94% of adjusted gross income (AGI) for households in the bottom 80% of the income distribution. Even for households in the 98th to 99th income percentile, wages and retirement income accounted for 71% of AGI.

At the very, very top, though, these sources are less important, accounting for just 15% and 7% of the income of the top 0.01% and the top 0.001% of households, respectively. These households receive most of their income from investments (interest, dividends, and especially realized capital gains) and businesses (including sole proprietorships, partnerships, and S corporations). These items constituted 82% of income for the top 0.01% and 88% for the top 0.001%, compared to just 7% for the bottom 80% of households.

LINK

Posted on 5/27/25 at 3:14 pm to mule74

quote:

I am talking about all taxes. Not just income taxes.

Which, makes your argument even sillier. And actually, you are talking about income taxes, you just don't realize it.

quote:

Again, you are only referencing income taxes. I am referring to all taxes.

Which again, makes your argument even less valid.

quote:

Most Americans receive almost all their income through wages and retirement income (pensions, 401(k)s, social security, and individual retirement accounts). The most recent available IRS data (2014) shows that wages and retirement income made up 94% of adjusted gross income (AGI) for households in the bottom 80% of the income distribution. Even for households in the 98th to 99th income percentile, wages and retirement income accounted for 71% of AGI.

At the very, very top, though, these sources are less important, accounting for just 15% and 7% of the income of the top 0.01% and the top 0.001% of households, respectively. These households receive most of their income from investments (interest, dividends, and especially realized capital gains) and businesses (including sole proprietorships, partnerships, and S corporations). These items constituted 82% of income for the top 0.01% and 88% for the top 0.001%, compared to just 7% for the bottom 80% of households.

Yes, yes, this isn't anything new. This isn't an argument that actual proves your point though. Sorry. These are also part of your income taxes, so your claim about talking about "all taxes" is incorrect. You claimed the middle class pays the highest effective rate. That is factually incorrect. You realize that capital gains, dividends, business income, etc are included in AGI right? So the effective rates paid factors this in.

In fact, the Treasury actually did a study looking at how things were broken out by wealth groups instead.

LINK

ETA: And if you really want to see a breakdown, based on AGI, here you go (2022 data):

The top 10% were responsible for 7,282,111 ($ Millions) of AGI (49% of all AGI), with an average effective rate of 21.11, and made up 72% of income taxes paid.

The Top 50% to 10% were responsible for 5,778,703 ($ Millions) of AGI (39% of all AGI), with an average effective rate of 9%. and made up 25% of income taxes paid.

LINK

This post was edited on 5/27/25 at 4:43 pm

Posted on 5/27/25 at 4:12 pm to GoCrazyAuburn

quote:

The top 10% were responsible for 7,282,111 ($ Millions) of AGI (49% of all AGI), with an average effective rate of 21.11, and made up 72% of income taxes paid.

The Top 50% to 10% were responsible for 5,778,703 ($ Millions) of AGI (39% of all AGI), with an average effective rate of 9%. and made up 25% of income taxes paid.

Are you suggesting the top 50% already pay 97% of the taxes? Those greedy bastards need to pay their fair share!!! I'm mad as hell they won't just pay more.

How is this thread not about expenses?

Posted on 5/27/25 at 4:18 pm to UpstairsComputer

quote:

Are you suggesting the top 50% already pay 97% of the taxes?

I'm not suggesting anything, the data proves this

quote:

How is this thread not about expenses?

Well, not trying to make this a politics discussion. From the financial side of things though, it will inevitably become unsustainable. Not discussing the rightness or wrongness of our tax brackets and fair share arguments, thats for the PT board. As far as this board is concerned though, as long as you have a disproportionate amount of your tax base not really contributing into the social works system that they are drawing from, it will inevitably fail. As evident, even Denmark is having to adjust their payout dates.

Yes though, at some point if the gorvernment is not going to spend your money responsibly and efficiently, the discussions must be had about why are we still giving to them.

Posted on 5/27/25 at 7:43 pm to Doctor Strangelove

quote:

They’re not even trying to hide it anymore. Most of the money we put into “social security” along with the amount our employers pays into our accounts will never be realized in our lifetime.

Well that’s not true at all. Based on average SS benefits and life expectancies, 65 y/o today in the US can expect around $480k in benefits over their lifetime. That is more than any current SS beneficiary has paid into it assuming they’re a W-2 employee. That’s actually 3x more than anyone who has maxed out SS for the last 45 years would have paid into it.

The math gets a little funny if you’re self employed and/or try to account for employer contributions, but SS is in trouble precisely because it cannot keep up with the money going out, not because people are getting less than they put in.

Page 2 of 4

Page 2 of 4

Popular

Back to top